The headlines have spoken - "GDP: It's official - we're in recession" and "New Zealand slips into double-dip recession amid rate hikes".

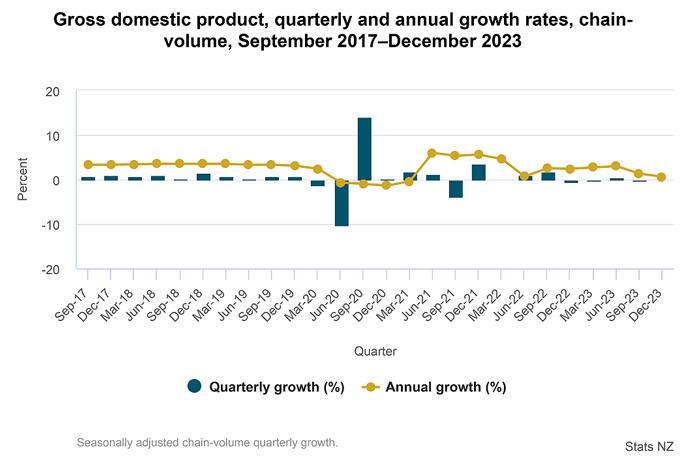

Stats NZ has said the economy contracted 0.3 per cent in the three months ended September, followed by a 0.1 per cent contraction in the December quarter.

In reality the economy has shrunk in four of the past five quarters, which included the lingering effects of Covid-19 restrictions.

But what is a recession and what is GDP? RNZ is here to clear it all up.

What's a recession?

Let's get the definition out of the way early.

Two consecutive quarters of negative growth (a paradox surely) are called a technical recession, a definition devised in the mid-1970s by a US bureaucrat, Julius Shiskin.

Only the US seems to have an official declaration of recession, which is done by the National Bureau of Economic Research.

A survey of economists last year by www.interest.co.nz found as many points of views and alternative definitions as participants, proof of George Bernard Shaw's quip that if all the economists were laid end to end, they'd never reach a conclusion.

But let's agree that New Zealand's economy as a whole has been going backwards for the best part of a year, even if the slowdown has been unevenly felt by people.

"Cue more talk about NZ re-entering technical recession. Technical recession or not (who knows, it could get revised away), to us the bigger picture remains the same. The economy continues to bump along the bottom," says BNZ head of research Stephen Toplis.

Photo: Stats NZ.

Photo: Stats NZ.What's gross domestic product (GDP)?

At best, it's an imperfect measure of all the value of the goods and services produced by an economy - from growing kiwifruit, mending broken cars and legs, building a house, selling big screen televisions or two-minute noodles, to the money spent on holding a general election or hiring a real estate agent .

In other words, a pick'n'mix of consumption, investment, government spending, and trade, and when adjusted for inflation it gives a broad measure of whether an economy is growing or shrinking, running hot or cold.

Although New Zealand talks about primary products being the backbone of the economy - the infant formula flooding into China, the kiwifruit on its way to Europe, the beef headed to US fast food chains - the reality is it accounts for about six per cent.

Industries and manufacturing accounting for 20 per cent, and services for the lion's share of 66 per cent, which is why when consumers stop spending, or buy the plain wrapped supermarket brand rather than the expensive imported brand, or don't replace the old pair of shoes, hold on to last year's mobile phone, and skip modernising the bathroom the economy has a palpitation.

GDP is a belated, rear-vision mirror view of the economy, which is bound to be revised. Indeed major revisions stretching back several years occurred in 2023 suggesting the economy had been weaker than previously thought.

Just numbers you might say, except they were the numbers the RBNZ was using to assess how fast or slow the economy was and whether they should be raising interest rates faster, slower, or not at all.

"The weakness we're seeing and feeling is all by RBNZ design. The RBNZ needs to restrain the economy in their fight against the inflation beast. And today they got that. Well, they got more than that," says Kiwibank chief economist Jarrod Kerr.

When you get away from the recession headlines and the big GDP numbers, there are indicators making it far more personal.

The per-capita GDP numbers give a partial pointer to our standard of living, our individual shares of the economic pie, and the latest Stats NZ numbers show it shrank 0.7 per cent in the past quarter, and close to three per cent over the past year, largely through the surge in migration.

In many respects, that number is the personal recession being felt by many households.

Is GDP the best measure?

Many argue no.

"GDP measures everything except that which makes life worthwhile," US Senator Robert Kennedy once said.

Its imperfections include not measuring health, education, equality of opportunity, voluntary work, the state of the environment or sustainability.

It tallies the value of the dairy products produced on New Zealand farms, but not the environmental cost of dirty rivers or methane emissions.

Alternatives are mooted based on happiness, wellbeing, sustainability. One finding some favour is the Genuine Progress Indicator (GPI).

It's been applied to New Zealand's economy with results suggesting the economy's not as well off as many think it is.

Regardless of how good or otherwise GDP is as a measure of growth and prosperity, it will not be toppled any time soon.

In May, the National-led government will publish its first Budget. GDP forecasts will be prominent either as stick to beat the previous government or as statement of ambition to get the country back on track.

1 comment

Excellent article.

Posted on 22-03-2024 12:27 | By morepork

One of the best I have seen on explaining these concepts. So, what do we do about it? If I ruled NZ, here's what I would do:

1. Immediately stop all immigration, except temporary visas for people to support fruit picking and harvests. This has nothing to do with Racism; it has to do with Economics. We simply don't have the infrastructure to support the levels of immigration which have been allowed. Time is needed for us to "catch up"and stabilise the Economy.

2. Use the standard controls (like managing interest rates) to control inflation (which simply robs all of us and makes saving pointless...)

Sadly, none of my oversimplified solution will be adopted because governments don't manage using reason, they manage using politics.

Leave a Comment

You must be logged in to make a comment.